California climate disclosure laws 2026: SB 253 deadline and SB 261 injunction

California climate disclosure laws in 2026: the proposed SB 253 deadline, SB 261 injunction, revenue thresholds and evidence companies need.

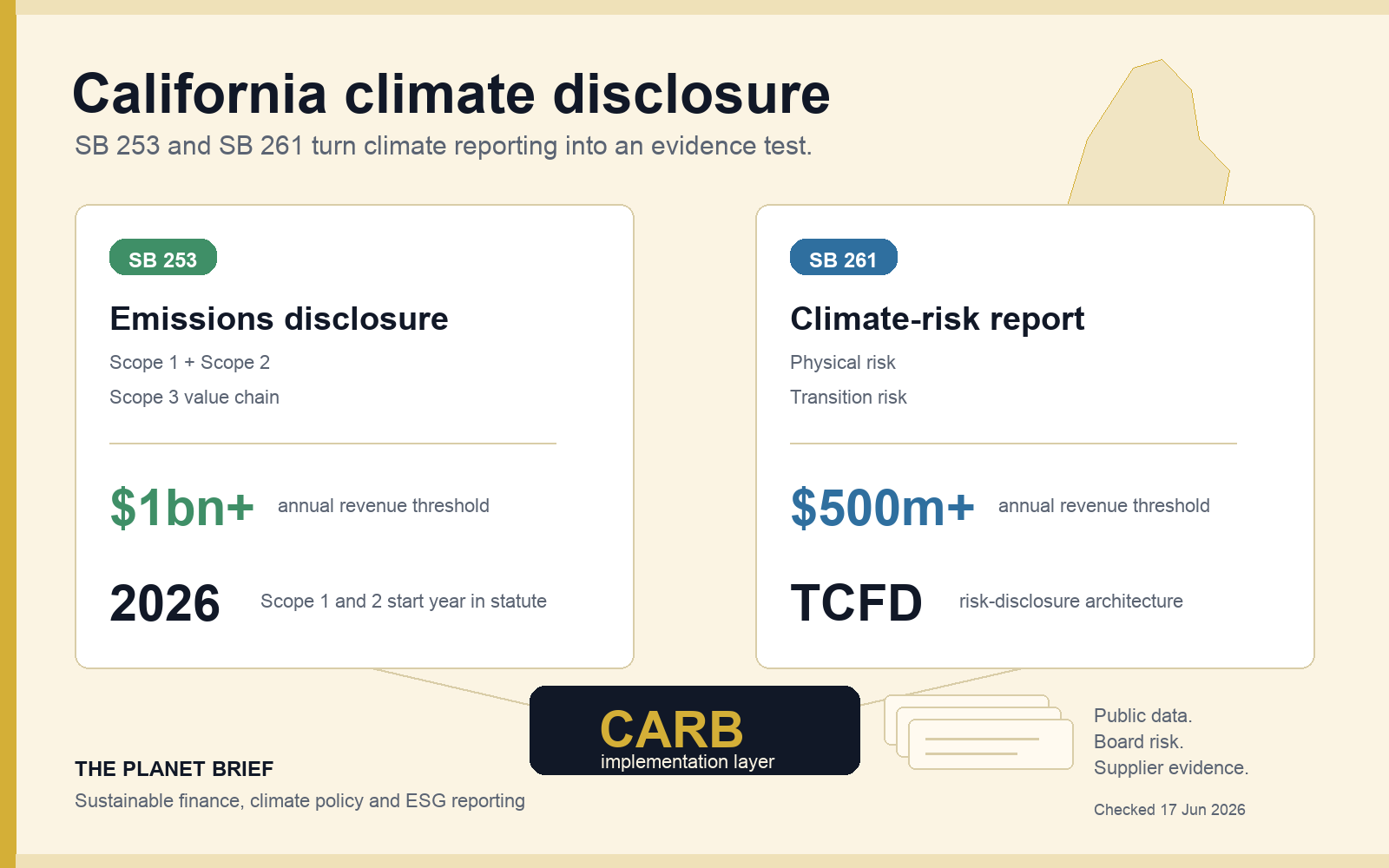

California's climate disclosure laws are moving on two different tracks in 2026. Senate Bill 253 (SB 253) emissions reporting is still advancing, although regulators have proposed moving the first deadline from 10 August to 10 November. Senate Bill 261 (SB 261) climate-risk enforcement remains paused under a court injunction.

For companies, the split matters more than the shared label. SB 253 creates an immediate data and assurance problem for large businesses preparing Scope 1 and Scope 2 reports. SB 261 asks a wider group to explain climate-related financial risk, but the California Air Resources Board (CARB) is not currently enforcing its reporting deadline.

The laws can still reach companies headquartered elsewhere because both use revenue thresholds and a doing-business-in-California test. Parent groups and private companies may therefore need a scoping review, while suppliers can feel the effect when customers ask for emissions data. The legal position depends on the final regulation, current court orders and each company's facts, but the underlying environmental, social and governance (ESG) evidence cannot be assembled at the last minute.

SB 253 advances while SB 261 remains paused

CARB approved an initial regulation in February with 10 August 2026 as the first SB 253 reporting deadline. It later withdrew the package from the Office of Administrative Law so that it could clarify parts of the regulation and open a further 15-day comment period. On 24 June, CARB said it would propose moving that deadline to 10 November 2026 before resubmitting the package.

The November date is therefore the regulator's proposed timetable, not yet a final effective deadline. The underlying SB 253 requirement has not disappeared: first-year reports cover Scope 1 and Scope 2 emissions, with Scope 3 reporting due to begin in 2027. CARB has also said it intends to use enforcement discretion for good-faith first-year submissions.

SB 261 is in a different position. A federal appeals court injunction prevents enforcement while litigation continues. Companies can still publish and voluntarily submit climate-risk reports, and CARB said in February that more than 120 had already been submitted, but it is not enforcing the January 2026 statutory deadline.

SB 253 and SB 261 at a glance

| Question | Short answer |

|---|---|

| What are California's climate disclosure laws? | SB 253 is the Climate Corporate Data Accountability Act for emissions disclosure. SB 261 covers climate-related financial risk reporting. |

| Who is in scope? | SB 253 applies to reporting entities with more than $1 billion in total annual revenue that do business in California. SB 261 applies to covered entities with more than $500 million in total annual revenue that do business in California, with insurance exclusions. |

| What is the first SB 253 deadline? | CARB has proposed moving the first Scope 1 and Scope 2 reporting deadline from 10 August to 10 November 2026. The revised regulation still needs to complete rulemaking and receive approval. |

| Is SB 261 being enforced? | No. CARB says it will not enforce SB 261 while a federal appeals court injunction remains in place. Voluntary public submissions continue. |

| What should companies prepare? | Start with entity scope, revenue and California nexus, then build traceable Scope 1 and Scope 2 data, an assurance file and a plan for Scope 3 supplier evidence. |

Revenue thresholds and 2026 dates

| Number or date | Where it fits | Why it matters |

|---|---|---|

| More than $1 billion | SB 253 revenue threshold | The emissions law targets very large reporting entities doing business in California. |

| More than $500 million | SB 261 revenue threshold | The climate-risk law reaches a wider group of large covered entities, subject to exclusions. |

| 10 November 2026 | Proposed first SB 253 deadline | CARB proposed a three-month deferral after withdrawing the initial regulation for limited clarification and resubmission. |

| 2027 | SB 253 Scope 3 start year in the statute | Value-chain data becomes the harder reporting problem because it depends on suppliers, customers, logistics and estimates. |

| More than 120 | Voluntary SB 261 reports submitted by February 2026 | Some companies continued reporting despite the enforcement injunction, creating an early public evidence base. |

| Up to $500,000 | SB 253 annual penalty cap in the statute | The emissions law has a much larger penalty ceiling than the risk-reporting law. |

| Up to $50,000 | SB 261 annual penalty cap in the statute | The risk-reporting law still creates a formal compliance exposure, even though the cap is lower. |

The threshold gap is easy to miss. SB 253 starts above $1 billion in revenue, while SB 261 starts above $500 million. A company can therefore sit outside the emissions-disclosure threshold while remaining within the climate-risk law's statutory scope, even though enforcement is currently paused.

SB 253 vs SB 261

The two laws are often discussed together, but they do different jobs. SB 253 is about measuring and disclosing emissions. SB 261 is about explaining climate-related financial risk.

| Feature | SB 253 | SB 261 |

|---|---|---|

| Main job | Public greenhouse gas emissions disclosure. | Public climate-related financial risk reporting. |

| Revenue threshold | More than $1 billion in total annual revenue. | More than $500 million in total annual revenue. |

| California link | Doing business in California. | Doing business in California. |

| Core content | Scope 1, Scope 2 and Scope 3 emissions. | Physical and transition risks that could harm financial outcomes, plus measures to reduce or adapt to those risks. |

| Reporting lens | Greenhouse Gas Protocol standards and guidance, unless an alternative standard is adopted later. | TCFD recommendations, successor framework or equivalent reporting requirement. |

| Assurance | Scope 1 and Scope 2 limited assurance begins with the first reporting cycle and reasonable assurance is scheduled from 2030 under the statute. Scope 3 limited assurance can begin from 2030 if CARB establishes it. | The statute is about public risk reporting, not emissions assurance. |

| Current 2026 status | Preparation continues. CARB has proposed 10 November 2026 for the first report, subject to final rulemaking and approval. | Enforcement is paused under a federal appeals court injunction; voluntary reports can still be published and submitted. |

| Public visibility | Public emissions disclosures through the reporting structure set by CARB. | Climate-related financial risk report made publicly available on the company's own website. |

SB 253 asks whether an emissions number is measured and supported. SB 261 asks whether the company understands what climate change and the transition could do to its financial position, operations, supply chain, investments or demand. In July 2026, the first question still has an approaching reporting cycle; the second sits behind an injunction.

SB 219 changed the timetable and reporting options

SB 219 is important because it changed several implementation details after SB 253 and SB 261 were signed. It did not remove the basic architecture. It made the machinery more flexible.

| Area | SB 219 effect | Why it matters |

|---|---|---|

| Regulation timing | CARB's regulation deadline for SB 253 became 1 July 2025. | The statutory design moved into a CARB implementation phase. |

| Where SB 253 reports go | Reports can go to the emissions reporting organization if one is contracted, or to CARB. | Companies should not assume the reporting channel until current CARB guidance is checked. |

| Scope 3 schedule | Scope 3 disclosure starts in 2027, but the schedule is to be specified by CARB. | The value-chain timetable is not only a fixed 180-day rule from the original text. |

| Parent consolidation | Reports may be consolidated at parent-company level where the statute allows. | Groups need to map entity structure, subsidiaries and revenue thresholds carefully. |

| SB 261 equivalent reporting | SB 219 added International Sustainability Standards Board (ISSB) Sustainability Disclosure Standards as one possible equivalent reporting route. | California risk reporting now sits closer to the global investor-focused disclosure baseline. |

The original SB 253 text is therefore only the starting point. A current scoping review also needs the SB 219 amendments, CARB's revised rulemaking package and the latest legal status.

Revenue and supply chains extend the reach beyond California

California's economy is large enough that a state-level rule can behave like a market-level rule. A company does not need to be a California brand to care. The practical trigger is whether a business is large enough, does business in California and fits the statutory definition after current guidance and advice are applied.

That makes the law relevant to several groups:

- large private companies that may not be caught by public-company climate disclosure regimes;

- public companies already preparing emissions, risk and investor disclosures;

- parent groups that need to understand whether consolidated reporting is possible;

- suppliers asked for emissions data by customers that may be in scope;

- finance, legal, audit, risk and sustainability teams that need one evidence file rather than separate narratives.

The supplier effect is especially important. SB 253 includes Scope 3 emissions, which means a reporting entity may need information from companies that are not directly in scope. For smaller suppliers, the first encounter with California climate disclosure may not be a regulator. It may be a customer questionnaire.

What companies control, share and depend on

The hardest work is not writing the final report. It is deciding which parts of the evidence chain the company controls directly, which parts it shares with others and which parts depend on estimates.

| Evidence area | Control level | Practical implication |

|---|---|---|

| Scope 1 fuel, refrigerants and owned operations | High control | Finance, facilities and operations teams should be able to trace data to bills, meters, logs or asset records. |

| Scope 2 purchased energy | High to medium control | Companies need electricity and energy records, locations, market-based instruments and method documentation. |

| Scope 3 suppliers, logistics, product use and travel | Shared or low direct control | The evidence file needs supplier data, reasonable estimates, calculation methods and a plan to improve data quality. |

| Climate-related financial risk | Shared across governance, finance and risk | The report should connect climate risks to operations, supply chain, assets, demand, capital, insurance and resilience. |

| Public claims and investor materials | High control | Marketing, annual-report and investor language should not outrun the underlying emissions and risk evidence. |

How one manufacturer would prepare

Imagine a fictional electronics company, Ridgeway Devices. It has $1.3 billion in annual revenue, sells into California, has a parent company with several subsidiaries and relies on contract manufacturers across Asia and North America.

Under SB 253, the obvious data is not enough. Ridgeway may have good Scope 1 data for company vehicles and facilities, and Scope 2 data for purchased electricity. The harder problem is Scope 3: purchased components, outsourced manufacturing, freight, business travel, product use and end-of-life treatment. The company needs a method that can use primary supplier data where possible and documented estimates where supplier data is weak.

For SB 261, the question changes. Ridgeway must think about climate-related financial risk: heat disruption in supplier regions, flood exposure at logistics hubs, carbon-cost exposure in materials, customer demand for lower-carbon products, energy-price volatility and the cost of redesigning products or supply chains. The injunction changes enforcement, not the usefulness of doing this work.

The same company therefore needs two linked workstreams: one produces emissions data, while the other explains how climate risk could affect the business. Their overlap tests whether finance, legal, risk, procurement and sustainability teams can explain the same story with the same evidence.

TCFD, ISSB and CSRD can support the evidence base

California's laws sit inside a crowded reporting landscape, but they are not identical to the European Union's Corporate Sustainability Reporting Directive (CSRD), the International Sustainability Standards Board (ISSB) baseline or UK climate disclosure rules.

They are also separate from the federal securities regime. The SEC climate disclosure rules guide explains the stayed 2024 rule, the Commission's 2026 repeal proposal and the materiality-based duties that remain in federal filings.

SB 261 is closest in shape to disclosure based on the Task Force on Climate-related Financial Disclosures (TCFD) because it asks for climate-related financial risk and measures adopted to reduce or adapt to that risk. The TCFD structure also lives on inside International Financial Reporting Standard S2 (IFRS S2) and other climate disclosure regimes.

SB 253 is closer to the emissions-data layer. It pushes companies toward a public greenhouse gas inventory covering direct emissions, purchased energy and value-chain emissions. That connects naturally to the Greenhouse Gas Protocol and to reporting regimes that ask for Scope 1, Scope 2 and Scope 3 evidence.

CSRD is broader because it uses double materiality and covers a wider set of sustainability topics. ISSB is investor-focused and built around sustainability-related financial disclosure. California's laws are narrower in topic but powerful because they apply by revenue and California business connection, not only by listing venue.

What a readiness file should contain

The safest first step is not a glossy sustainability report. It is a readiness file that proves the company knows its scope, data, owners and gaps.

- entity structure, parent company and subsidiary map;

- California business-nexus review and revenue-threshold analysis;

- emissions boundary and consolidation approach;

- Scope 1 and Scope 2 activity data sources;

- Scope 3 category map, assumptions and supplier-data plan;

- assurance-provider readiness and evidence controls;

- climate-risk register linked to operations, supply chain, assets and finance;

- governance owners across finance, risk, legal, audit, procurement and sustainability;

- public website and report-publication process;

- claims review so public sustainability language matches the evidence.

That file does not decide every legal question. It gives decision-makers something solid to work from when CARB guidance, assurance expectations, legal status or customer requests change.

Disclosure evidence also governs public claims

California climate disclosure also changes the claims environment. Once emissions and climate-risk information become more public, broad claims about climate leadership, low-carbon products, net zero readiness or resilient supply chains become easier to test against reported data.

That does not mean companies should stop communicating. It means claims need narrower boundaries and better evidence. If a company says it is reducing emissions, readers should be able to see which scope, which baseline, which method and which part of the value chain is included. If a company says it is resilient to climate risk, the risk report should not describe severe exposures with no credible response.

The reporting lesson and the green-claims lesson are the same: evidence comes before language.

One evidence base, two reporting duties

California's climate disclosure laws are best understood as a two-part accountability system. SB 253 asks large companies to disclose emissions across operations, purchased energy and value chains. SB 261 asks large companies to explain climate-related financial risk.

The strongest companies will not treat that as two separate reports. They will treat it as one evidence problem: who is in scope, what data exists, who owns the risk, what can be assured, and whether the public story matches the underlying facts.

Common questions about SB 253 and SB 261

Are SB 253 and SB 261 the same law?

No. SB 253 covers emissions disclosure, while SB 261 covers climate-related financial risk. They overlap in audience and governance but ask different reporting questions.

Does SB 253 require Scope 3 emissions?

Yes. The statute covers Scope 1, Scope 2 and Scope 3 emissions. Scope 3 reporting starts in 2027 under the statute, with the schedule specified by CARB as part of implementation.

Is 10 November 2026 the final SB 253 deadline?

Not yet. CARB announced that it would propose moving the first deadline from 10 August to 10 November 2026, then resubmit the clarified regulation for approval. Companies should monitor the final rulemaking rather than treating the proposed date as settled.

Do California climate disclosure laws apply to private companies?

They can. The statutory thresholds refer to business entities with specified total annual revenue that do business in California, rather than only to public companies. The exact scope should be checked against current guidance and advice.

Is TCFD still relevant to SB 261?

Yes. SB 261 references the Task Force on Climate-related Financial Disclosures recommendations or an equivalent reporting requirement. TCFD remains useful because its governance, strategy, risk management, and metrics and targets structure still shapes climate-risk reporting.

Can an ISSB report help with SB 261?

Potentially. SB 219 added ISSB Sustainability Disclosure Standards as one possible equivalent reporting route for climate-related financial risk reporting. Companies still need to check whether their report satisfies current California requirements.

What should companies do first?

Start with scoping and evidence. Map entities, revenue thresholds, California nexus, emissions boundaries, data owners, Scope 3 suppliers, climate-risk governance and public-reporting processes before drafting the final disclosure.

Useful source links

- CARB: June 2026 notice proposing the SB 253 deadline deferral

- CARB: California corporate climate disclosure rulemaking page

- CARB: SB 261 voluntary reporting docket and injunction notice

- California Legislative Information: SB 253 Climate Corporate Data Accountability Act

- California Legislative Information: SB 261 climate-related financial risk

- California Legislative Information: SB 219 amendments

- Greenhouse Gas Protocol: standards and guidance

- IFRS Foundation: IFRS S1 General Requirements

- IFRS Foundation: IFRS S2 Climate-related Disclosures

- Task Force on Climate-related Financial Disclosures: recommendations

- Wikimedia Commons: California State Capitol image by Andre m, CC BY-SA 3.0

{kind=link}

Data checked

Checked 20 July 2026 against CARB's corporate climate disclosure rulemaking page, its notice proposing a move to 10 November 2026, its SB 261 injunction and voluntary-docket notice, and official bill text for SB 253, SB 261 and SB 219. The proposed SB 253 deadline still depends on final rulemaking and approval, while the SB 261 enforcement position can change with the litigation.

Information only

Una comparación útil de camisetas de fútbol versión aficionado comienza por el peso del tejido, la ventilación y la elasticidad. El pedido puede cerrarse después de confirmar qué versión aparece exactamente en las fotografías.

This guide is for general information only. It is not legal, accounting, regulatory, investment or financial advice. Companies should check current California Air Resources Board (CARB) guidance, litigation status and professional advice before making compliance decisions.

Know this subject well? Send evidence, corrections or a useful lead to hello@theplanetbrief.com.