EU ESG ratings regulation 2026: why supervised scores will still disagree

EU ESG ratings regulation 2026 explained: what Regulation (EU) 2024/3005 changes for ESG rating providers, investors, companies, methods and conflicts.

The European Union (EU) environmental, social and governance (ESG) ratings regulation started applying on 2 July 2026. It does not make every ESG score converge. It makes rating providers answerable for their methods, conflicts and governance, so a score becomes easier to inspect instead of easier to trust blindly.

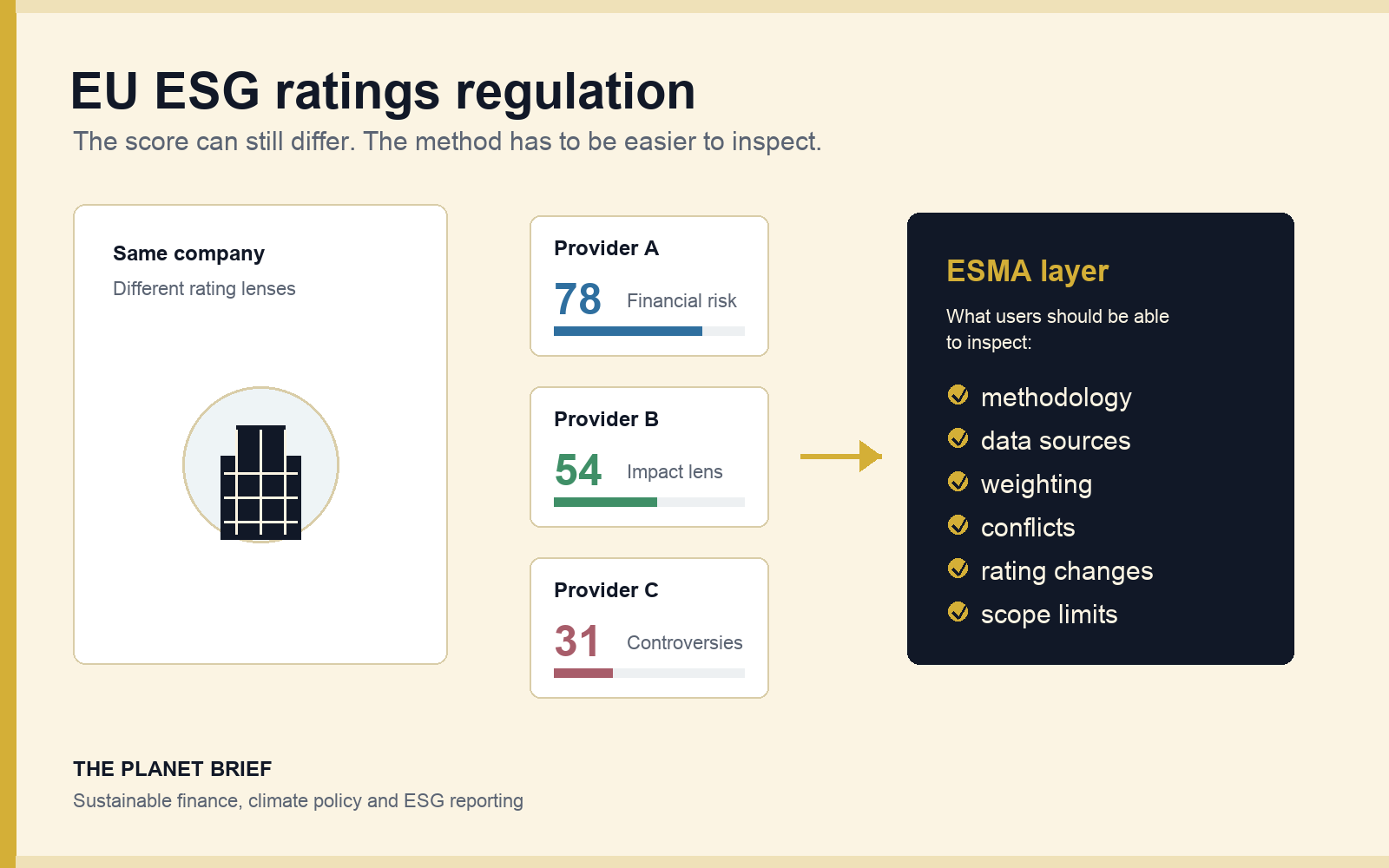

ESG ratings have a reputation problem because they often disagree. One provider may rate a company highly because it manages financially material risks well. Another may rate the same company lower because it gives more weight to controversies, social issues, governance weaknesses or environmental impact.

The new regime brings a messy ratings market into a supervised perimeter through transparency, governance and conflict-management rules. It neither creates a single official ESG score nor promises that ratings will stop disagreeing.

A rating can shape fund selection, index construction, stewardship, lending conversations, issuer engagement and public claims. If users do not know what the score measures, how it is weighted, what data feeds it and where conflicts sit, the rating can look more objective than it really is.

The EU ESG ratings regime at a glance

| Question | Short answer |

|---|---|

| What is the EU ESG ratings regulation? | Regulation (EU) 2024/3005 is the EU rule on the transparency and integrity of ESG rating activities. |

| Who supervises ESG rating providers? | The European Securities and Markets Authority (ESMA) is the direct supervisor for providers offering ESG ratings in the EU. |

| When does it apply? | It started applying on 2 July 2026. ESMA's notification and authorisation process then becomes the practical test. |

| Will ESG scores become identical? | No. Providers can still use different methods, but users should get more transparency about those methods and conflicts. |

| What should users do now? | Ask what the rating measures, how it affects a decision, what changed since the last score and which conflicts are disclosed. |

| Why does it matter? | Ratings influence sustainable finance, fund research, issuer access to capital and greenwashing risk, so the evidence behind them matters. |

ESMA supervision changes how providers operate

The EU regulation brings ESG rating providers that offer services in the EU into a formal regulatory perimeter. Providers need to register, become authorised or use another permitted route into the EU market, depending on their status. ESMA says providers offering ESG rating services in the EU need to notify it if they intend to continue operating, then submit an authorisation or recognition application where required.

For users, the most important point is not the paperwork. It is the change in information discipline. The regulation is designed to improve transparency, integrity and governance around ESG ratings. That means more attention to methodology disclosure, conflicts of interest, organisational separation and the way ratings are produced and distributed.

The rule does not decide that one methodology is correct. A climate-risk score, a broad ESG score and an impact-oriented score can still answer different questions. But under a stronger regime, the provider should be clearer about which question it is answering.

The regulation does not turn ESG ratings into truth. It makes the basis of the rating harder to hide.

Application and authorisation dates

| Item | Figure or date | What it means |

|---|---|---|

| Regulation | Regulation (EU) 2024/3005 | The EU law covering transparency and integrity of ESG rating activities. |

| Date of application | 2 July 2026 | The date from which the ESG Ratings Regulation starts applying. |

| Provider notification deadline | 2 August 2026 | Existing providers that want to keep operating in the EU should notify ESMA by this date, unless a specific small-provider route applies. |

| Application deadline for existing providers | 2 November 2026 | The regulation gives existing providers four months from 2 July 2026 to apply for authorisation or recognition. |

| Small provider temporary regime | Three years | Small providers based in the EU may use a temporary regime if they meet size criteria. |

Those dates make 2026 an operating year, not just a rulebook year. Providers have process work to do. Users have a different task: find out which ratings they rely on, whether those ratings sit inside the EU regime and what provider disclosures will now be available.

Why ESG ratings disagree

ESG ratings disagree because they do not all measure the same thing. Providers may focus on financially material risk, broader impact, disclosure quality, sector-relative performance or controversies, and they can assign very different weights to governance, climate exposure and labour issues.

The famous problem is often called "aggregate confusion". Florian Berg, Julian Koelbel and Roberto Rigobon documented that ESG ratings diverge because providers differ on scope, measurement and weighting. In plain English, they choose different issues, measure those issues differently and combine the results differently.

| Reason ratings differ | What the user should ask |

|---|---|

| Scope | Which ESG topics are included and which are excluded? |

| Measurement | Which data points, estimates, controversies and disclosure fields are used? |

| Weighting | How much does each topic affect the final score? |

| Materiality lens | Is the rating about financial risk, real-world impact, or a mix of both? |

| Data freshness | How quickly does the rating update after new disclosures or controversies? |

The regulation cannot remove all disagreement because some disagreement is legitimate. A climate-transition-risk model and a broad stakeholder-impact model should not always produce the same result. The problem is not difference itself. The problem is unexplained difference.

Providers must disclose methods and manage conflicts

The regulation pushes providers toward more visible methods and stronger organisational controls. A user should expect more attention to how a provider defines an ESG rating, what data sources it uses, how it manages conflicts, how it separates rating work from other business activities and how it explains material changes.

ESG rating providers can sit in complicated commercial positions. A group may sell ratings, data, benchmarks, consulting or other services. A provider may rate a company while also selling data products to investors who hold that company. A conflict does not automatically make a rating wrong, but hidden conflicts make the rating harder to use well.

For investors and companies, the practical question is simple: if the score changed, could the provider explain why?

A useful rating file should make the following visible enough for a serious reader:

- the purpose of the rating;

- the main ESG themes included;

- the data sources and estimation approach;

- the weighting logic;

- the role of controversies or incidents;

- the update cycle;

- the conflicts policy;

- the limits of the rating.

Supervision will not produce one official ESG score

Regulation will not make an ESG rating objective in the same way as a temperature reading because a rating turns incomplete and contested information into a score, category or opinion. Providers can make different reasonable choices, so supervision can improve transparency and integrity without removing judgement from the methodology.

The rule also does not turn ESG ratings into investment recommendations. A strong ESG rating does not make a security cheap, diversified, suitable, low risk or high impact. A weak ESG rating does not automatically mean a company is uninvestable. Financial risk, valuation, portfolio role, costs, time horizon and investor objectives still matter.

Finally, the regulation does not replace corporate reporting rules such as the Corporate Sustainability Reporting Directive (CSRD), the International Sustainability Standards Board (ISSB) baseline or the Sustainable Finance Disclosure Regulation (SFDR). Ratings sit on top of company data, market data and provider judgement. Better underlying disclosure may improve ratings quality, but it is not the same thing as regulating the rating provider.

Investors need to know how a score enters the portfolio

Investors often encounter ESG ratings through fund factsheets, index rules, platform screens, portfolio tools and manager reports. The rating can look like a simple quality signal, but it may be doing a narrower job.

A fund may use ESG ratings to exclude low-ranked companies, tilt portfolio weights or inform active research, while another manager may build an internal framework and ignore provider scores. The same rating can therefore have very different consequences depending on its role in the investment process.

The regulation should help users ask better questions. It should be easier to distinguish a rating that measures sustainability-related financial risk from a rating that tries to capture broader impact. That distinction is crucial for anyone comparing Article 8 funds, Article 9 funds, UK Sustainability Disclosure Requirements (SDR) labels or broad ESG funds.

Investor check

Do not ask only whether a fund uses ESG ratings. Ask which provider it uses, what the rating measures, how much the score affects holdings, whether the manager can override it and whether the fund documents explain those choices clearly.

Companies gain a clearer route to challenge factual errors

Companies often experience ESG ratings as a black box. They disclose information, respond to questionnaires, receive a score and then face questions from investors, lenders or customers. If the score is low, it may not be obvious whether the problem is missing data, a real performance weakness, a controversy, sector exposure or a methodology choice.

A more transparent ratings regime should make the conversation cleaner. Companies should be better able to understand what kind of evidence affects a score, whether the methodology rewards disclosure quality, how controversies are treated and how often updates happen.

That does not mean companies should manage only to the rating. The better approach is to build credible sustainability evidence that can survive several lenses: regulation, investor due diligence, customer procurement, public claims and rating provider methodology.

In practice, the strongest company response is not to chase every score. It is to know which ratings matter to key investors or customers, identify recurring data gaps, keep source evidence organised and make sure public claims match the underlying information.

Read the score through its objective and method

A stronger regime does not remove the need for judgement. It gives readers more material to judge.

| Reader question | Why it matters | Warning sign |

|---|---|---|

| What does the score measure? | Financial risk, impact and disclosure quality are different questions. | The score is treated as a general "good company" badge. |

| What changed since the last rating? | Method changes, new data and controversies can all move the score. | The provider or fund cannot explain the movement. |

| How is the score used? | A small research input is different from a binding index rule. | The fund says it uses ESG ratings but gives no portfolio effect. |

| What conflicts exist? | Ratings, data, benchmarks and other services can sit in the same group. | The provider gives little detail on conflict management. |

| What is outside the rating? | A rating may miss topics that matter to the reader's decision. | The rating is used as a substitute for holdings or issuer analysis. |

Ratings sit downstream of disclosure and fund rules

ESG ratings regulation is one piece of a wider sustainable-finance rulebook. It sits beside, not above, other regimes.

The Sustainable Finance Disclosure Regulation (SFDR) is about sustainability-related disclosure for financial products and financial market participants in the EU. The Sustainability Disclosure Requirements (SDR) regime is the UK investment label and disclosure framework. The Corporate Sustainability Reporting Directive (CSRD) is the EU corporate sustainability reporting regime. International Sustainability Standards Board (ISSB) reporting standards are used as a global baseline for sustainability-related financial disclosure. The ESG ratings regulation targets the information intermediaries that turn company and market data into ratings.

That means a fund can be classified under SFDR and still use a third-party ESG rating. A UK product can use an SDR label and still use external research. A company can report under CSRD and still be scored differently by different providers.

The pieces do different jobs. CSRD and reporting based on ISSB standards improve the raw disclosure layer. SFDR and SDR govern how financial products explain sustainability claims. The ESG ratings regulation governs part of the ratings layer that investors and products may use to interpret that information.

There is another naming layer too. If a fund name itself uses ESG or sustainability-related terms, the ESMA fund naming guidelines help explain when the name needs stronger portfolio evidence.

Transparency improves the score without standardising it

The EU ESG ratings regulation will not make every score converge, and it will not turn ratings into investment advice. Its value is narrower and still important: it makes a powerful information layer more visible, supervised and accountable.

The reader's job is still to ask what the rating measures. The regulation should make that question easier to answer.

Common questions about EU ESG ratings regulation

What does ESG stand for?

ESG stands for environmental, social and governance. It is a broad framework for analysing issues that can affect companies, funds, risk, resilience and sustainability claims.

Who regulates ESG rating providers in the EU?

ESMA, the European Securities and Markets Authority, is the direct supervisor for ESG rating providers offering services in the EU under Regulation (EU) 2024/3005.

Does the EU ESG ratings regulation make ratings comparable?

It should make methods, conflicts and provider governance easier to inspect, but it does not force every provider to use the same methodology or produce the same score.

Are ESG ratings the same as credit ratings?

No. Credit ratings assess creditworthiness. ESG ratings can assess sustainability characteristics, ESG risks, impacts or a mix of factors depending on the methodology.

Should investors rely on one ESG score?

No. A score can be useful as a starting signal, but investors should still check holdings, methodology, fund objectives, costs, risks, exclusions, stewardship and relevant disclosures.

Useful source links

- ESMA: ESG rating providers

- EUR-Lex: Regulation (EU) 2024/3005

- European Commission: ESG rating provider registration fee delegated regulation

- ESMA: legislative action on ESG ratings and assessment tools

- Review of Finance: Aggregate Confusion, The Divergence of ESG Ratings

Data checked

Checked 20 July 2026 against ESMA's ESG rating providers page, Regulation (EU) 2024/3005 and the Review of Finance paper on ESG rating divergence. The regulation has applied since 2 July 2026; existing providers face notification and authorisation deadlines during 2026. Review after material authorisation updates, fee changes, provider registers, questions and answers or supervisory guidance.

Information only. This guide is general information. It is not legal, regulatory, investment or financial advice, a recommendation or a personal financial promotion. ESG ratings, fund labels and provider documents can change.

Know this subject well? Send evidence, corrections or a useful lead to hello@theplanetbrief.com.